TL;DR:

- Plumbing insurance is a specialized policy that protects homeowners from costly plumbing failures and water damage. It covers sudden leaks, blocked drains, emergency repairs, and some heating system issues, but excludes gradual wear, maintenance neglect, and faulty work. This insurance fills the gaps left by standard home policies, especially regarding slow leaks and emergency call-outs, offering financial security and quick access to qualified plumbers.

Plumbing insurance is a specialised form of cover designed to protect homeowners from the financial impact of plumbing failures, water damage, and emergency repair costs. Unlike standard home insurance, it targets the specific risks that come with pipes, drains, and heating systems. Water damage claims average between £11,098 and £13,954 per incident for homeowners. That figure alone explains why understanding this cover matters before a problem strikes, not after. This guide covers plumbing insurance explained in plain terms: what it covers, what it excludes, how it differs from your home insurance, and how to choose the right plan.

What does plumbing insurance cover?

Plumbing insurance is not a single product. It is a collection of coverages grouped under one umbrella, and the components you need depend on your home, your risk profile, and your existing policies. Knowing what sits inside a typical policy stops you from paying for gaps you did not know existed.

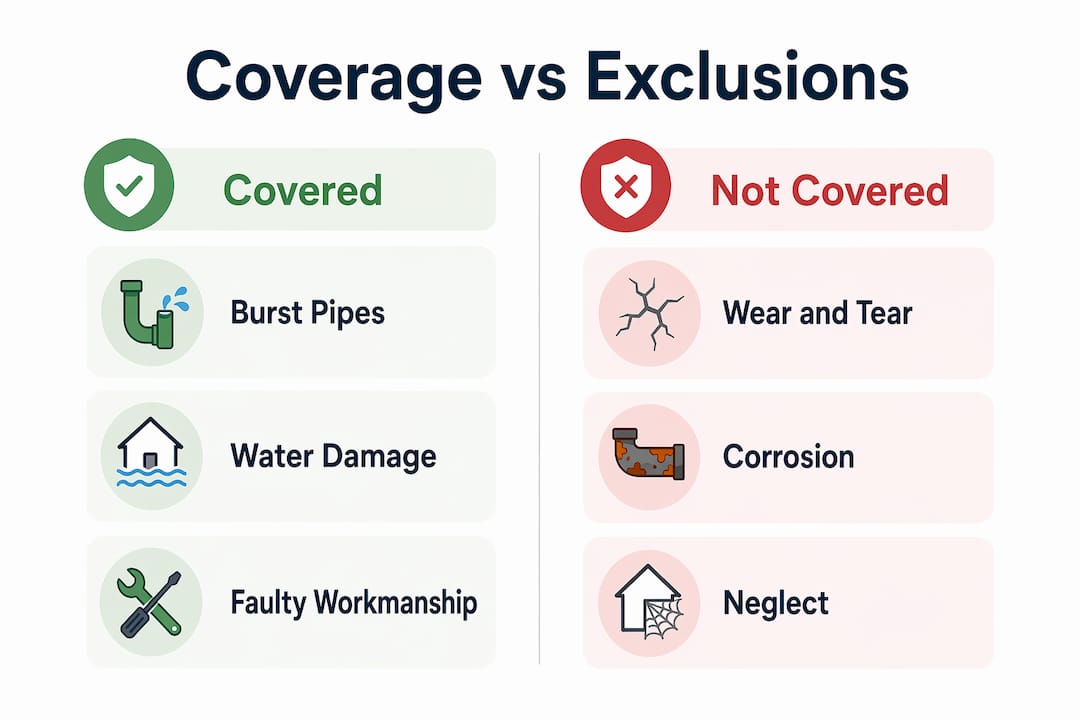

Most standard plumbing insurance policies cover the following:

- Burst pipes and sudden leaks. Damage caused by a pipe that fails without warning, including the cost of tracing the source and repairing the surrounding structure.

- Blocked drains and drain repairs. Clearance of blockages and repair of damaged drain sections, including external drains in many policies.

- Water damage remediation. Drying out, replastering, and restoring areas damaged by an insured plumbing event.

- Emergency call-out costs. Labour and parts for urgent repairs, often with a 24-hour helpline included.

- Boiler and heating system cover. Some plans extend to central heating pipework, though boiler cover is frequently sold separately by providers such as British Gas and HomeServe.

Exclusions are where most homeowners get caught out. Common exclusions include gradual wear and tear, corrosion, maintenance neglect, and the cost of redoing faulty plumbing work. This last point is known as the "your work" exclusion. It means the policy will pay for damage caused to your property by a failed repair, but it will not pay the plumber to redo the job itself. Sewer backups and chemical contamination are also typically excluded from standard policies, though pollution liability cover can be added for around £800 to £2,400 annually.

Annual claim limits and aggregate caps vary widely between providers. Always check the maximum payout per incident and the total annual limit before signing.

Pro Tip: Read the exclusions section of any policy before the coverage section. Insurers write exclusions in precise legal language. If you are unsure whether gradual pipe corrosion or a slow leak is covered, call the provider and ask them to confirm in writing.

How does plumbing insurance differ from home insurance?

This is the question most homeowners get wrong, and the misunderstanding can cost thousands of pounds. Homeowners insurance covers plumbing damage only when the cause is sudden and accidental. A pipe that bursts overnight qualifies. A pipe that has been slowly corroding for two years does not.

The table below shows the key differences:

| Scenario | Standard home insurance | Plumbing insurance |

|---|---|---|

| Burst pipe (sudden) | Usually covered | Covered |

| Slow leak or gradual corrosion | Excluded | Often covered (check policy) |

| Blocked drains | Excluded | Covered |

| Plumber's faulty workmanship damage | Not directly covered | Covered via completed operations |

| Emergency call-out costs | Not included | Included in most plans |

| Water damage restoration | Covered if cause is covered | Covered |

The distinction around a plumber's faulty workmanship is particularly important. When a plumber causes damage to your home, your insurer may pay your claim and then pursue the plumber's insurance through a legal process called subrogation. Most plumbing liability claims begin with exactly this process, where your insurer seeks reimbursement from the plumber's completed operations cover. If the plumber you hired is uninsured or underinsured, that recovery process fails, and you may be left with an uncovered shortfall.

This is why checking that any plumber you hire carries adequate public liability insurance is not just a formality. It directly affects your financial protection if something goes wrong after the job is done.

Pro Tip: Before hiring any plumber, ask for proof of their public liability and completed operations insurance. A reputable tradesperson will provide this without hesitation. If they cannot, find someone who can.

What are the benefits of plumbing insurance for homeowners?

The practical benefits of plumbing insurance go beyond simply paying a repair bill. For most UK homeowners, the value sits in three areas: financial certainty, access to qualified tradespeople, and protection against the unpredictable nature of ageing pipework.

-

Financial protection from large, unexpected costs. Emergency plumbing repairs and water damage restoration are among the most expensive unplanned home costs. A single burst pipe can require replastering, flooring replacement, and mould treatment on top of the plumbing repair itself. Insurance converts an unpredictable large expense into a manageable monthly premium.

-

Access to vetted, insured contractors. Providers such as HomeServe and British Gas operate networks of approved engineers. When you claim, they send a qualified professional rather than leaving you to find one in an emergency at 11pm on a Sunday.

-

Peace of mind for older properties. Homes built before the 1970s often have copper or lead pipework that is more susceptible to failure. Regular plumbing inspections help identify risks early, but insurance provides the financial backstop when an inspection misses something or a failure occurs between checks.

-

Cover for the gaps in your home insurance. As the comparison above shows, standard home insurance leaves meaningful gaps around gradual damage, blockages, and emergency call-outs. Plumbing insurance fills those gaps directly.

-

Simplified claims process. Many plumbing cover plans operate as service contracts rather than traditional insurance policies. You call a helpline, they arrange the repair, and you pay nothing beyond your monthly fee up to the policy limit. This removes the paperwork burden of a standard insurance claim.

When choosing a plan, weigh the coverage limit against the age and complexity of your plumbing system. A newer build with modern plastic pipework carries less risk than a Victorian terrace with original cast-iron drains. The cost of plumbing insurance should reflect that risk profile, not just the cheapest headline premium.

Common misconceptions about plumbing insurance coverage

The biggest misconception is that home insurance already covers everything plumbing-related. Homeowners frequently assume their buildings policy handles all plumbing issues, which leads to uncovered losses and disputed claims. The reality is that standard home insurance is designed for sudden structural events, not the slow, incremental failures that cause the majority of plumbing problems.

A few other misunderstandings are worth addressing directly:

- "All water damage is covered." Water damage is only covered if the cause of the damage is a covered event. If a slow leak caused by poor maintenance damaged your floor over six months, most standard policies will reject the claim entirely.

- "The plumber's insurance is my problem." It is not your problem until it is. If a plumber causes damage and their insurer disputes the completed operations claim, you will be waiting for a resolution while living with the damage.

- "Newer homes do not need plumbing cover." New builds carry their own risks, including poorly fitted joints, substandard materials, and drainage issues that emerge within the first five years.

- "Maintenance does not affect my cover." It does. Failure to maintain your plumbing system is one of the most common grounds for claim denial. Regular inspections and documented maintenance records strengthen your position if you ever need to make a claim.

"The most expensive plumbing claim is the one you thought was covered but was not. Read your policy before you need it, not while you are standing in two inches of water."

Key takeaways

Plumbing insurance fills the coverage gaps that standard home insurance leaves open, protecting homeowners from the full financial cost of plumbing failures, water damage, and emergency repairs.

| Point | Details |

|---|---|

| Plumbing insurance defined | It is specialised cover for plumbing failures, water damage, and emergency repairs beyond standard home insurance. |

| Home insurance limitations | Standard policies cover only sudden, accidental damage and exclude gradual leaks, blockages, and maintenance-related failures. |

| Completed operations cover | Damage caused by a plumber after leaving your property is covered by their completed operations insurance, not yours. |

| Exclusions to watch | Wear and tear, maintenance neglect, and the cost of redoing faulty work are excluded from most plumbing policies. |

| Choosing the right plan | Match coverage limits and provider reputation to your home's age, pipework type, and existing insurance gaps. |

Why plumbing insurance deserves more attention than it gets

Most homeowners I speak with have never read the plumbing section of their home insurance policy. They assume it is covered. When a claim is rejected because a leak was deemed "gradual" rather than "sudden," the surprise is genuine and the financial pain is real.

What strikes me most is how the insurance industry has structured this gap almost invisibly. Home insurance sounds comprehensive. The word "buildings" suggests the whole structure is protected. But the exclusions around maintenance and gradual deterioration mean that the most common type of plumbing failure, the slow, unnoticed leak, is precisely what most policies do not cover.

The providers doing this well, HomeServe and British Gas among them, have built service models that remove the ambiguity. You pay a monthly fee, you call a number, someone comes. That simplicity has real value for homeowners who do not want to become experts in policy wording.

My honest view is that plumbing cover is worth having for any home over 15 years old, and worth reviewing annually as your property ages. Pair it with a professional plumbing inspection every two to three years, keep records of any maintenance work, and you are in a far stronger position both to prevent claims and to win them when they arise.

— Michael

Protect your home with the right plumbing support

Understanding plumbing insurance is the first step. Having a reliable, insured plumber on call is the second.

Your-local-plumber provides fast, transparent plumbing services across the UK, carried out by experienced engineers who carry full public liability insurance. Whether you are dealing with an emergency repair or want a routine inspection to keep your insurance valid, the team is ready to help. Browse the completed work gallery to see the standard of service you can expect, and get in touch to discuss your plumbing needs with a local specialist who understands what your insurer will want to see.

FAQ

What is plumbing insurance for homeowners?

Plumbing insurance is a specialist policy that covers the cost of repairing or replacing plumbing systems damaged by leaks, burst pipes, blockages, and related water damage. It fills the gaps left by standard home insurance, which typically excludes gradual damage and emergency call-out costs.

Does home insurance cover plumbing repairs?

Home insurance covers plumbing damage only if the cause is sudden and accidental, such as a pipe bursting overnight. Gradual damage, corrosion, and maintenance neglect are excluded from most standard buildings policies.

How much does plumbing insurance cost in the UK?

Costs vary by provider, property age, and coverage level. Service plan providers such as HomeServe and British Gas offer monthly plans starting from around £5 to £20 per month for basic plumbing cover, with more comprehensive packages costing more.

What is completed operations cover and why does it matter?

Completed operations coverage protects against damage caused by a plumber's work after the job is finished. It matters to homeowners because if a repair fails and causes water damage days later, this is the coverage that pays, not your standard home insurance.

Do I need plumbing insurance if I already have home insurance?

Yes, in most cases. Home insurance leaves significant gaps around gradual leaks, blocked drains, and emergency call-outs. Plumbing insurance or a dedicated service plan covers these gaps and provides access to qualified engineers without the need to source them yourself in an emergency.